Your Eames Chair Is Not a Birkin

Luxury fashion has gone parabolic. Another luxury category has taken a nosedive.

Jean-Noël Kapferer and Vincent Bastien’s canonical book on luxury, The Luxury Strategy, defines luxury as follows:

“Premium means pay more, get more in functional benefits. Luxury is elsewhere. It signals the capacity of the buyer to transcend needs, functions, or objective benefits. This is how luxury brands are different from premium or super premium brands. Beyond the experience, they bring creative power, heritage, and social distinction.”

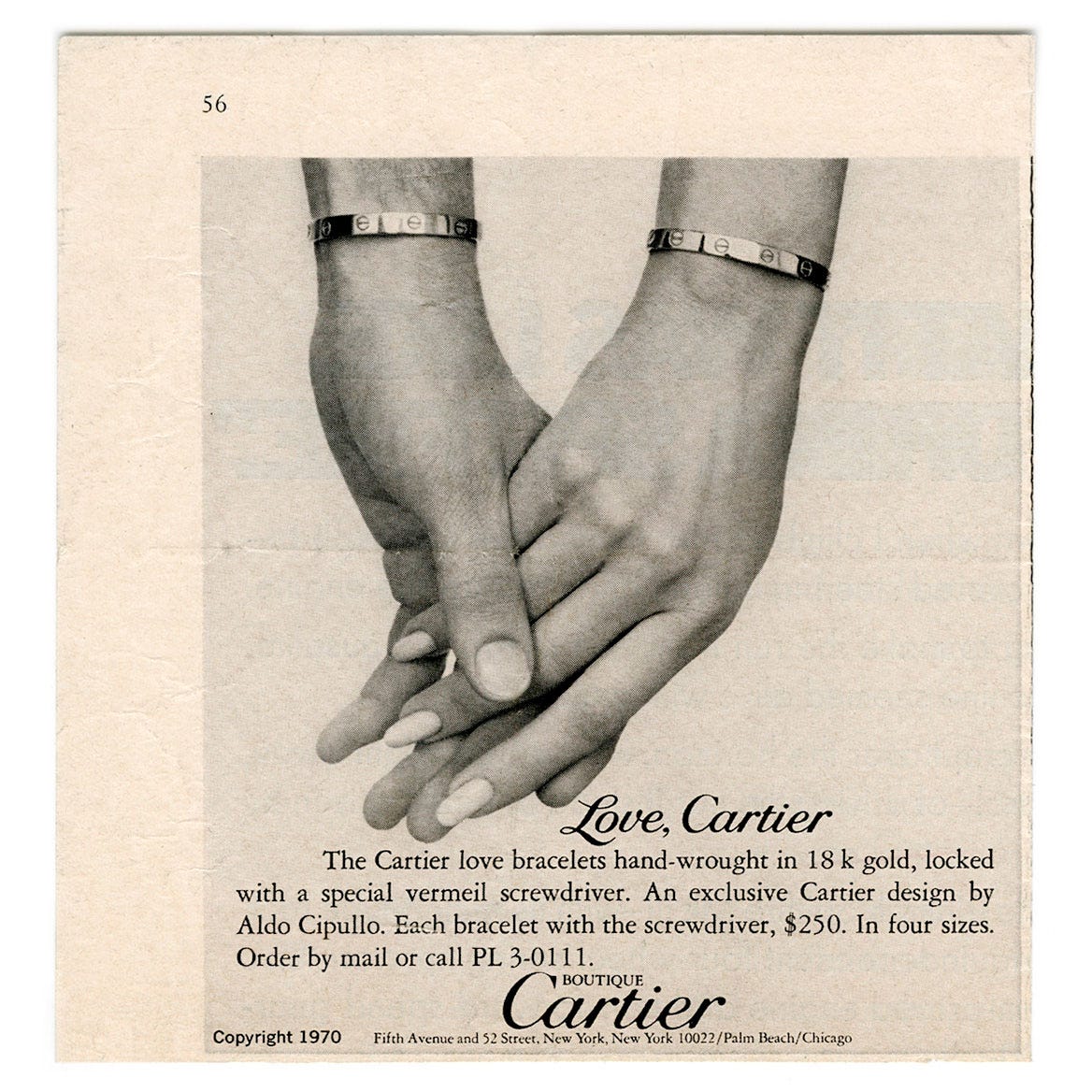

To notice that the luxury market—and specifically the market for luxury fashion and accessories—has seen parabolic growth in the last several decades is not exactly an original insight. However, the market has taken a novel shape. Take the Cartier Love Bracelet for instance; the 178 year old jeweler, acquired by Richemont in 1993, has been making this item for over half a century.

At $250 at the time and ~$2150 in inflation adjusted terms, this was a true luxury, especially in an era where the top decile of income was meaningfully smaller than it is today. Nonetheless, accounting for inflation, the present day price has nearly tripled, the amount of gold in the band has substantially decreased, and they are produced en-masse. This is a traditional observation of the luxury market: a fundamental increase in demand has been heralded by growing upper class incomes and visibility in the internet age. In turn, brand consolidation and professionalization on the supply-side means greater quantities on increasing margins can be sold.

These net income margins of luxury brands typically sit between twenty and thirty percent. The more exclusive, the higher they go. The question thus emerges: why would consumers pay that? The most best thesis I’ve found was posited by Ben Gilbert, one of the hosts of the Acquired Podcast. As he said:

“I think the most compelling argument around why luxury needs to exist is that it is a deeply human thing to signal your standing in the world. Everybody signals it in different ways. Now this is one of the infinite ways that someone could choose to signal to the world. This is not only what I choose to identify with taste-wise, but if you know, you know, especially with something like the Hermes Birkin bag, where it’s not marked. You’ll notice Louis Vuitton has LVs everywhere, but there are other brands that choose not to brand something, so that only people in the tribe can understand why it’s so valuable and luxurious. I totally buy the argument that it’s an essential part of humanity.”

In other words, humans have an innate need to signal their power to other humans, so they buy items that have intangible value (history, scarcity, etc) or are simply superfluous. You’re saying “Hey, look, I don’t need to buy things just for their benefits. I just buy things stuff at high prices because I can, and it shows that I have a discerning eye!”

The Cartier Love Bracelet is a perfect encapsulation of that. Such has been the case for luxury items across the board: fashion and accessories, specifically handbags and watches for women and men respectively have seen exponential increases in both demand and price. While out of reach for some urban professionals, luxury vehicles, too, have seen considerable inflation adjusted increases in price. Similarly, demand and market size have both exploded.

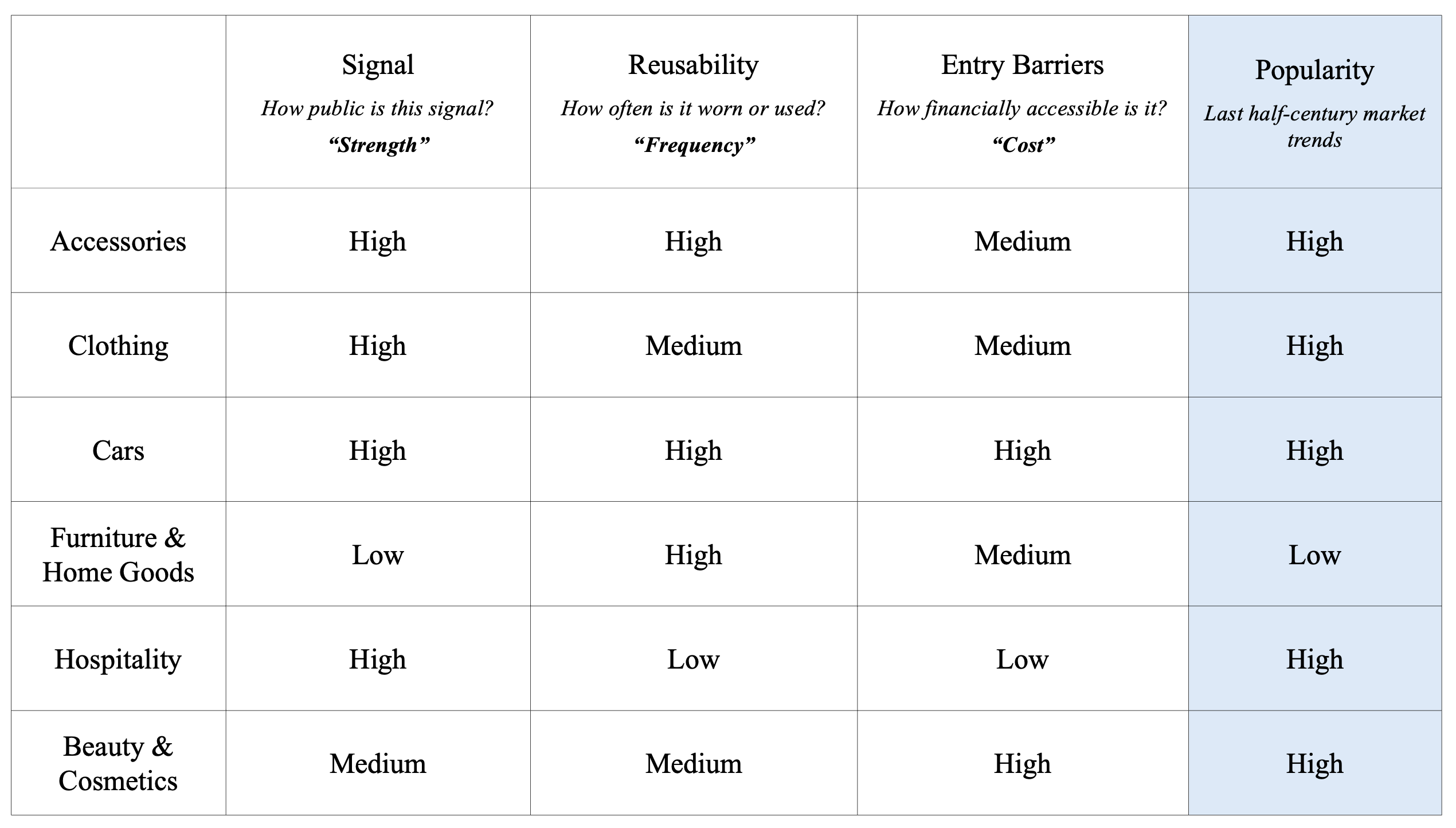

These items are notable for two things: primo, their perceived utility exists almost exclusively outside the home. They are viewed in public, and returned to their rightful place in a drawer or garage upon completion of signaling. Secondo, the main class of goods that is sold is frequently reusable. Accessories can be worn repeatedly, allowing for higher perceived value from the customer and increased margins for the manufacturer. When contrasted with clothing, it’s a critical distinction and explains why so much of luxury’s revenue derives from handbags, sunglasses, watches, and jewelry.

We can thus consider the luxury market across three key metrics: signal, reusability, and of course, entry barriers (otherwise known as cost):

One category stands out here: furniture and home goods. For Gen-Z, Millenials, and even some Gen-X who are not heirs to the discerning New York-Aspen-Palm Beach jet setting crowd (that is, the .01%, or termed here as NAPs), concern for the home has collapsed. Furniture and wall art are no longer top of mind; some in-demand pieces from a half century ago (e.g. original brown furniture or OBF, pewter) have seen their prices approach zero. While midcentury modern furniture has been spared such a decline, interest in it too has diminished, with buyers primarily composed of Boomers.

Some might attribute this to the rise of “fast furniture.” As Ingvar Kamprad, the founder of Ikea, famously wrote in The Testament of a Furniture Dealer:

“We shall offer a wide range of well-designed, functional home furnishing products at prices so low that as many people as possible will be able to afford them.”

Through him and many others (Wayfair, Amazon, etc), access to decent cheap furniture has been democratized. Nonetheless, this downshift in quality and price can be said to inaccurately reflect the habits of white-collar Americans in the last few decades. Increasingly, more time is being spent at home, not less. It is also contrary to the trends of many other categories: fast fashion at Zara and (relatively) cheap skincare at Sephora has coincided with the aforementioned exponential rise of luxury fashion and skincare.

With absolutely no evidence beyond notional conversations, I would posit that knowledge of basic staples of American home luxury from the mid to late 20th century (e.g. an Eames or Barcelona chair) has considerably diminished among Gen-Z and Millennials.1 Meanwhile, knowledge of luxury items across all other categories has exploded (Rolex, for instance, went from 20% to 80% brand awareness from 1978-98). From all of this—the proliferation of fast furniture and increasing knowledge and demand for luxury with the exception of home goods—I would add in one more personal experience: the Stubborn Boomer Supply Glut.

Most long-time owners of luxury home goods expect commensurate increases in price in line with inflation, or in some cases, other (more desirable) luxury goods. Most of these owners are old; they are Boomers who either bought this furniture or inherited it from their parents. Increasingly, they are aging, downsizing, and getting rid of it. Yet their perception of value is wholly divorced from the market price. And they’re very stubborn on this. They would rather hoard than sell.

How do I know this? Over the past several months, I’ve been to about a dozen of these high-end antique furniture markets (I’ve been in the market for some items, but also absolutely captivated by this phenomenon). The prices are astronomically high (nothing is under $500; many items are over $10k). Almost no one buys. I would estimate that they turn their inventory every 4 years, at most. In other words, Boomer stubbornness has created an immense supply glut that is only going to only expand for the foreseeable future.

Thus, we encounter one of the single-most bizarre and paradoxical market dynamics I’ve ever seen. Notional demand and a growing supply controlled by a disparate collective united in decentralized price fixing. As Will Manidis noted on X, the prices in Europe have to a certain extent cratered.2

I can confirm: shopping auctions at places like the UK based Mallams yields some of the best deals you’ll find (if you can ship it to the states at a reasonable price). Yet in the US, such prices remain extraordinarily high. I can only hope that they too go into free fall soon enough. To that end, in the next twenty five years, I would expect one thing for certain, and two things to plausibly occur:

The supply glut will grow, and stubborn Boomers can only hold out until they’re dead. We’ll slowly see this market crater over the next two decades (“slowly, and then all at once”).

[Seems likely] As evidence mounts that housing prices are directly correlated to supply (duh), and localities begin to loosen zoning restrictions owing to growing Gen-Z and Millenial pressure for cheaper housing, young urban professionals will again have more space and money to spend on their home. With the supply glut and oversaturation of “slop” furniture, demand for it will meet this increasing supply.

[Perhaps even more likely] As luxury conglomerates (LVMH, Kering, etc.) saturate fashion and accessories, they’ve increasingly turned to buying into hospitality (LVMH’s foray into this at Chez L’Ami Louis in Paris, is, as always, overpriced and excellent). However, the margins are simply not the same as handbags. Where they are the same is luxury furniture. I would expect them to place major bets in this market in the forthcoming years (in the form of a MillerKnoll buyout for instance, which, it happens, is trading at the lowest since the financial crisis).3

Until #1 happens, you can find me painstakingly combing through antique shops upstate in Hudson or driving over to the East Bay on my weekends, only to haggle with unrelenting Boomers and going home distraught and empty handed. I guess, if you’re old and unrelenting, you can just do things too.

At the very least, relative to their increasing knowledge of other luxury goods, i.e. if knowledge of an Andiamo handbag has 10x’d, we could expect knowledge of an Eames Chair to 2x perhaps, simply owing to the proliferation of information on the internet. Meanwhile, less popular luxury goods (e.g. OBF) has seen utter collapse.

Though I wholeheartedly dispute the notion that the next Larry Ellison will be an antique furniture dealer.

I know a lot of this piece (not to mention this assertion) has been upheld by scant evidence. I plan to write a piece in the future where I drill into the statistics on these markets as part of a full $MLKN value piece. If you made it this far, any reading suggestions would be much appreciated.